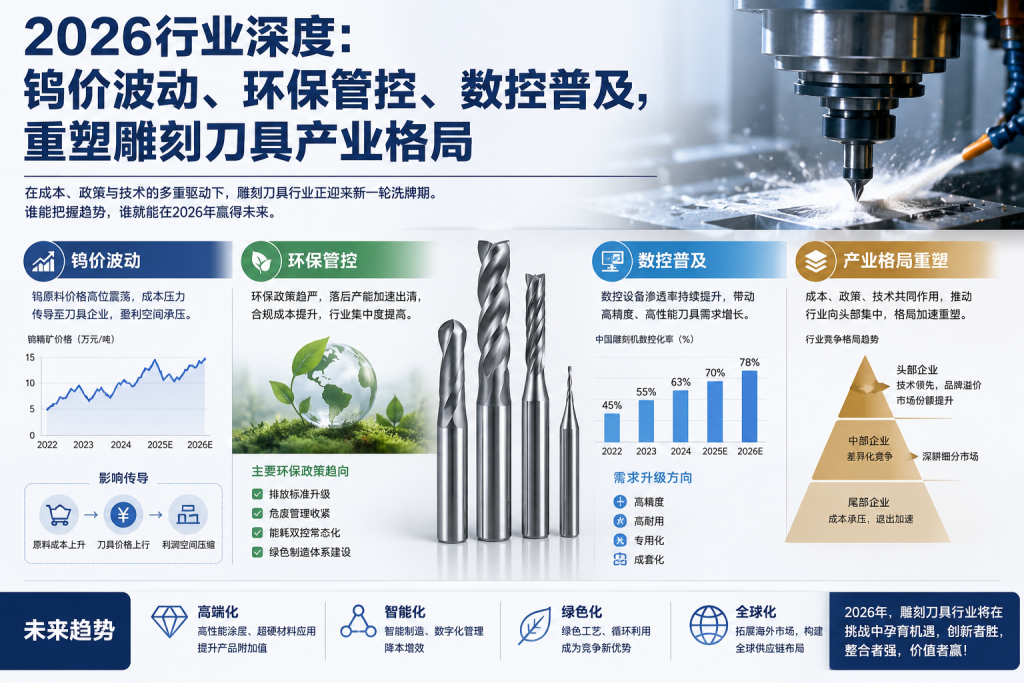

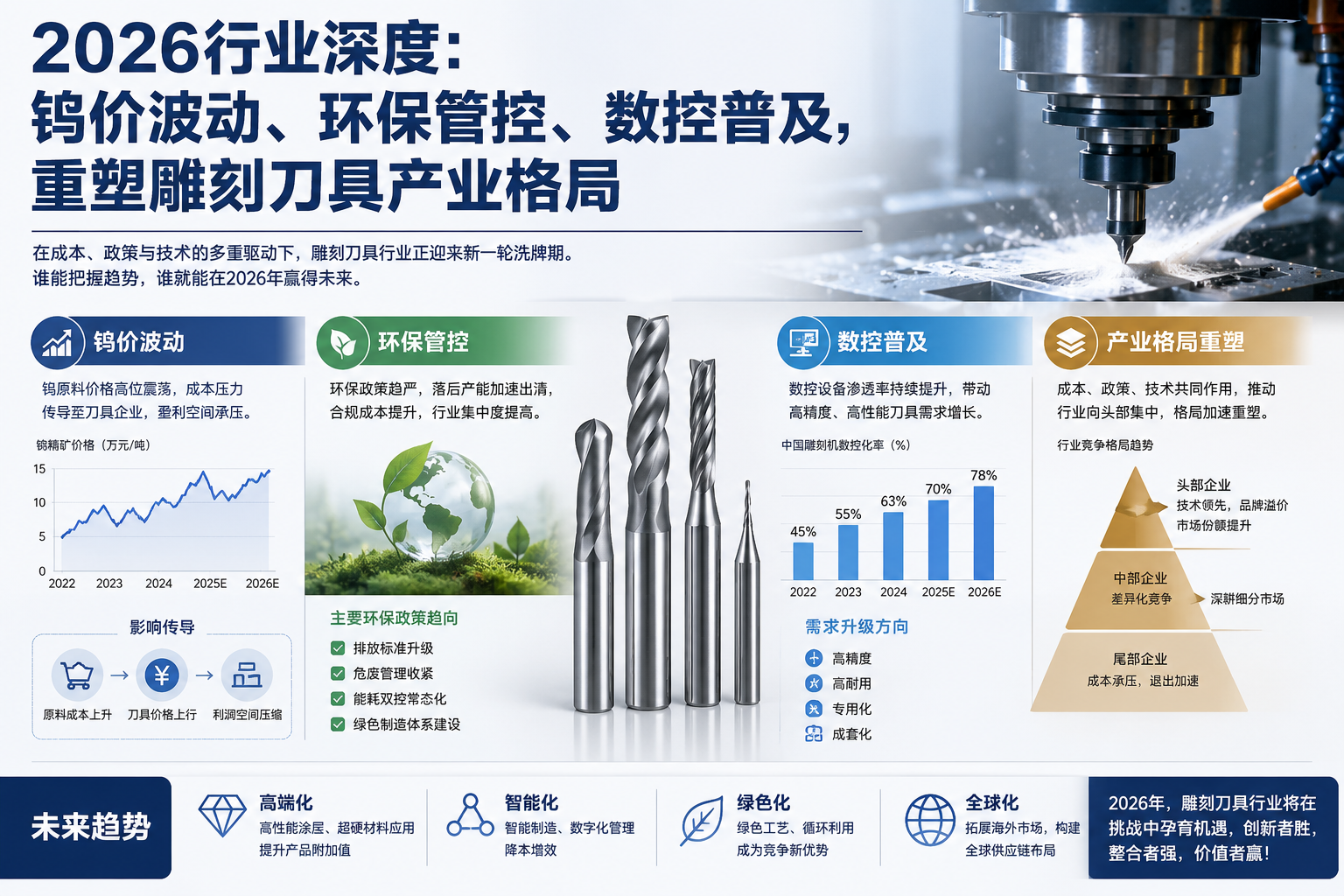

In 2026, the carving tool industry will enter a deep reshuffle stage, driven by three factors: significant fluctuations in tungsten prices, tightening of environmental policies, and comprehensive popularization of CNC equipment. The industry will completely bid farewell to low price and extensive competition, and usher in structural upgrading and pattern reshaping.

The price of tungsten raw materials is experiencing severe fluctuations, leading to the restructuring of the industry’s cost system. Tungsten carbide is the core raw material of hard alloy cutting tools, and its price has fluctuated significantly in the past two years, directly compressing the profit margins of small and medium-sized manufacturers. Most small workshops lack the ability to lock raw material prices and hedge inventory, resulting in a continuous decline in gross profit margins and accelerated clearance of low-end homogeneous production capacity. At the same time, the industry is accelerating material iteration, and the demand for low tungsten alloys, ceramic cutting tools, and PCD diamond cutting tools is rapidly increasing. Modular cutting tools with interchangeable heads are gradually replacing integral tungsten steel cutting tools, effectively reducing downstream processing consumables costs and becoming the mainstream direction for cost reduction in the industry. Top enterprises, with the advantage of upstream and downstream integration, continue to strengthen their cost and pricing discourse power, and accelerate the pace of domestic substitution.

Overall, the era of low-end internal competition in the carving tool industry has come to an end. In the future, the market will focus on material upgrading, green technology, precision manufacturing, and segmented matching. The localization of mid to high end products, new material matching, and foreign trade going global will become the core growth track of the industry in 2026.