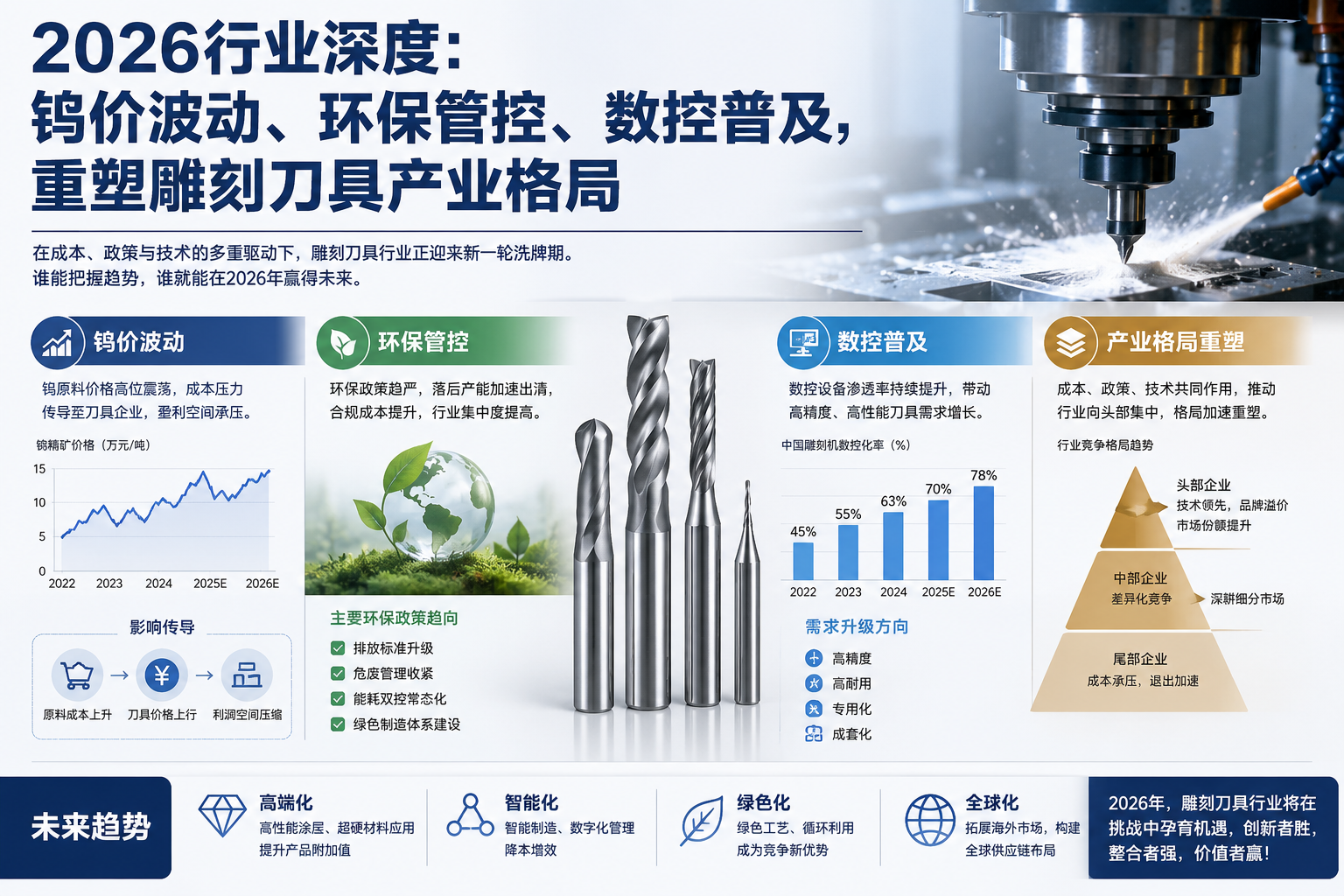

In 2026, the domestic carving tool industry will enter a structural adjustment cycle, influenced by three core factors: tungsten price fluctuations, environmental upgrades, and the popularization of CNC equipment. The market will accelerate the survival of the fittest, and the industry will officially bid farewell to the era of low price competition and transform towards high-end, refined, and green direction.

The fluctuation of raw material prices has become the primary driving force for industry changes this year. Tungsten carbide is the core raw material for carving tools, and its price continues to fluctuate, greatly reducing the profit margin of small and medium-sized tool enterprises. Most small processing plants lack raw material reserves and price locking capabilities, and can only passively compress profits in the face of rising costs. The gross profit margin of low-end general cutting tools continues to decline. In this context, the industry is accelerating material iteration, and the application of low tungsten alloys, ceramic cutting tools, PCD diamond cutting tools, and replaceable modular cutting tools is rapidly expanding, effectively reducing the cost of consumables for enterprises and becoming the new mainstream in the market. Top domestic enterprises with upstream industrial chain layout have obvious cost advantages, further accelerating the pace of import substitution.

At the same time, the normalization of environmental protection supervision continues to raise the entry threshold for the industry. With the implementation of policies such as VOCs control, new pollutant management, and carbon emission statistics, traditional high pollution spraying and outdated sintering processes are gradually exiting the market. The industry is fully implementing green processes such as PVD environmentally friendly coatings, vacuum sintering, and clean production. A large number of small workshops without environmental qualifications and outdated equipment are accelerating their clearance. The concentration of the industry continues to increase, and large-scale and compliant production has become the industry’s hard standard.

The comprehensive popularization of downstream CNC equipment has also forced the rapid upgrading of tool products. The automation level of whole house customization, advertising signage, rock slab stone, and new energy processing continues to improve, and traditional white steel cutting tools are completely eliminated in high-speed precision machining scenarios. The demand for high-precision coated tungsten steel cutting tools and specialized superhard cutting tools continues to grow. The market has shifted from general cutting tools to specialized, non-standard customized, and long-lasting wear-resistant precision competition.

Industry analysis points out that by 2026, the pattern of the carving tool industry will intensify, low-end production capacity will continue to clear, and the space for the mid to high end market will further open up. In the future, technology research and development, green production, precision manufacturing, and customized services will become the core competitiveness for enterprises to seize the market.

-1024x819.png)

.png)